In this week’s episode of Retire in Texas, Darryl Lyons, CEO and co-founder of PAX Financial Group, dives into the evolving concept of retirement, particularly for Generation X. Darryl challenges the traditional notion of retirement and explores the idea of pivoting rather than retiring, urging listeners to reconsider the inherent value of work. He discusses the unique financial challenges facing Gen Xers, from the 401(k) experiment to the changing landscape of Social Security, and emphasizes the importance of saving not just for retirement but for life’s unexpected turns.

Key show highlights include:

- The evolving definition of retirement and why “pivoting” might be a better approach.

- A conversation about the unique financial challenges facing Generation X.

- The connection between work, happiness, and personal well-being.

- The importance of saving for unforeseen life events, rather than just traditional retirement.

- A historical perspective on Social Security and its relevance to today’s longevity trends.

Tune in for an insightful discussion that challenges the conventional narrative around retirement and offers practical advice for planning your financial future. If you like this episode, be sure to share with a friend or family member!

PAX Podcast Ep. 145 – Transcript

Hey, this is Darryl Lyons, CEO and co-founder of PAX Financial Group. And you’re listening to Retire in Texas. This information is general nature only. It’s not intended to provide specific investment, tax or legal advice. Visit PAXFinancialGroup.com for more information.

Hey, and if you want to meet with one of our advisors who do have hearts of a teacher, then go to our website and connect with us and you’ll schedule a 15-minute conversation just to see if it’s a good fit. And it’s usually over the phone, it can be Zoom. But just a really good way to say, “Hey, here’s what I’m looking for. Tell me if you can help with this. If not, no problem.” But that’s just a really easy way just to see if this is a good fit. So it’s a connect button at PAXFinancialGroup.com for more information.

So, you know, I mentioned this before, but when we define retirement, by definition it means the disposal of an asset when it’s no longer useful. So, that’s what retirement means. Retire. I’m going to retire something. I’m gonna retire a piece of equipment. But it means this asset is no longer useful. And so, of course, when we talk about retirement from a human perspective, that doesn’t make sense to me.

That’s why you’ve often heard me say, “I don’t want you to retire. I want you to pivot.” But, you know, I’m often wondering, have we been oversold on this idea of retirement? Now, here’s where I’m going to have you go, just to kind of, you know, think a little deeper here. Would you conclude that if you believe in retirement, by default, you don’t believe that work is good?

So let me ask that again. Would you conclude that if you believe in retirement, by default, you don’t believe that work is good? Now that’s an extreme view point. And I know there’s a lot of gray in there. But I think it’s worth unpacking and asking ourselves, do we have a position? Do we have a conviction on whether or not work is inherently moral or immoral?

Now, the reason this becomes a little problematic by not resolving this is because as we go into an election year, this position on work, our position, our thoughts, and our convictions on work actually directly ties to public policy. A candidate’s view on whether or not work is good for a person or a family or society is important. Work, and when somebody works, they actually take pride in their craftsmanship and, and enjoy the bonding that takes place when you’re shoulder to shoulder with another person. Some politicians view work as only a mechanism to satisfy basic needs in life. So, which one do you choose?

Look at an Indian reservation and there’s many in many reservations that would prefer to work, despite the subsidies that cover all of their basic needs. But what position do you choose? Is work inherently good? Because we do have a retirement crisis in our country. And I think when we talk about retirement crisis, we can actually connect the dots between retirement and work a little bit better, and have a better way to – whether I think we are, I always have to ask myself, even if I do go through this intellectual exercise, what does it really mean to me? It does dictate how you vote, but it also dictates how you live life and how you teach the next generation. But when we see the headlines and you’ll see them all the time, now that I mentioned, it’s like a blue Ford truck, you’re going to see a blue Ford truck all the time.

But retirement crisis, you’re going to see this headline all the time. Retirement crisis. Retirement crisis. Is this country doomed because people at age 65 have to work? Are we doomed? Is it a crisis because a group of people have to work past age 65? Is that a bad thing? In fact, most studies I’ve read about work says that it leads to a better life in terms of happiness and satisfaction.

This is from the Harvard Business Review, one of the most robust findings in the economics of happiness is that unemployment is destructive to people’s well-being. And we find this true around the world. The employed evaluate the quality of their lives much more highly on average, as compared to the unemployed. Individuals who are unemployed also report around 30% more negative emotional experiences in their day to day lives.

Now, let’s drill down just a little bit more. And I’m actually going to not talk about the baby boomers for once. Look, you’re a baby boomer, you’re always getting the attention. Yes, Social security will be there. Yes, Medicare will be there. I know, you’re nervous about it, but they’re not going to, they’re not going to mess it up for your generation. They’re going to mess it up for The Goonies, the Gen Xers, the Karate Kid generation. For those of us who actually listened to Pearl Jam and liked it. Those that are born between 1965 and 1980, about 65 million people, were the 401(k) experiment.

You know, baby boomers, they got that Social Security pretty much reliable. Some of them, some of the baby boomers have some pensions, really don’t have to deal with student loan debt. Some of them work for the sheriff department, the post office, get a nice income. Didn’t overextend themselves. Did pretty good with their money. Again, not everyone. But juxtapose that with the Gen X, kind of an experiment on retirement. And a lot of the Gen X, well, they’re turning 60 soon, and they’re not going to be able to retire.

Is this a crisis? Feels like a little bit if you’re 60 and your kids are coming back home and your parents are aging and you don’t have that pension, and you got a late start on your 401(k) because of student loans. You know, think about it, the 401(k), the whole tax code of 401(k) didn’t actually start till 1978. And the Roth didn’t even start till 1997. So the experiment is still like, “Okay, we are just now realizing as a generation that cashing out your 401(k) to buy a car was probably a bad idea.”

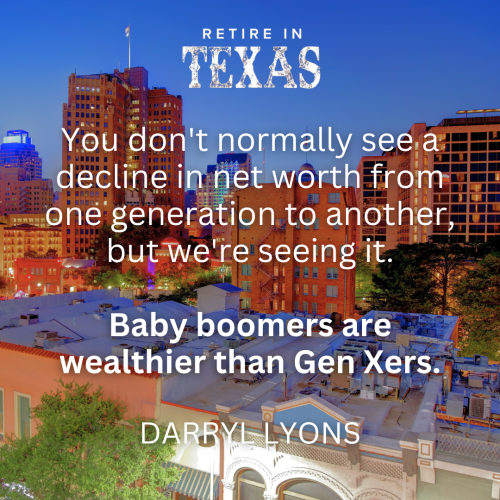

And many in the generation Gen X are still kind of like freaking out from 2008. In fact, what’s interesting about the Gen X is that the median, this is according to Federal Reserve. The median household net worth of Gen Xers between 45 and 54, this is in 2022, was about $250,000. And if you measure that against the baby boomers in that same age group at the same time of life, it’s 7% lower. So, you don’t normally see a decline in net worth from one generation to another, but we’re seeing it. Baby boomers are wealthier than Gen Xers.

So, do Gen Xers have a retirement crisis looming? It’s a crisis if you think work is bad. But I think what we’re going to see is a lot of Gen Xers pivot. I really do. I think you’ll see them. Some of them will be YouTubers. Yes, that is a business now. I mean, we can make fun of it, but it’s a legit business. Is there longevity in it? That’s a question. Because once the fad runs out, what do you do? But it is. Business consulting. I mean, the consulting is very much a niche. Going back to school is very much an option. Gen Xers may not be able to retire, but I don’t know if that’s bad. As long as you consider work good.

So, does that mean that Gen Xers should not save? Absolutely not. But for different reasons. I’m convicted that Gen Xers need to save, and I don’t know if I would have had that same level of conviction when I first started, but based on my experience now, it’s so important. And it’s not to save because I want you to simply retire and be disposed of an asset because you’re no longer useful. I want you to save because life happens.

I had a client years ago at 55. He was, he worked in the medical business, made $300,000 a year at 55 got dementia. His plan was just to start squirreling money away because he had done what a lot of us do and didn’t save in our younger years. So now his income was bigger, his shovel was bigger, so to speak, and he was going to start shoveling money aside and started forgetting so much he couldn’t work anymore.

Had he had a bucket of money, call it retirement money, the stress that his family experienced would not have existed to the same degree that it did. It was a, I walked alongside life with him, it was horrible. I want Gen Xers to save because work may not be an option. Now that’s if you’re white collar. If you’re blue collar, it’s a little bit more obvious, you’re like “My back will not let me do this forever.” Or, my dad who installed fire suppression systems, he’s like, “I can’t climb these ladders forever.” It’s a little easier when you see, when you see it physically, and you’re like, “Okay, there’s an ending point here.” And you can say, “Okay, I need some money when I can no longer do this with my hands.” If you have calluses on your hands. But if you’re white collar, that’s not as easy.

You think, “Well, I’m going to be able to do this forever.” But you just don’t know if a stroke or dementia will occur. And so you do need Gen Xers, that bucket of money, the just in case money. You can call it retirement money. You call it pivot money. I like to call it pivot money. Call it whatever, you know. But just know that we are living longer. And therein lies a problem. Worst case scenario, you can’t work anymore. Dementia, fall off a ladder, and you live to 100 and your kids are taking care of you. Or even worse, the state is taking care of you for 30 or 40 years of life. The CDC says that life expectancy is 77.5 years now. It went down a little bit with Covid. Interesting.

So, a 45-year-old female. Doesn’t smoke. Has pretty good health. About a 20% chance that she’ll live to age 100. 20% chance that she’ll live to age 100. So, Gen Xers, so you’re saying there’s a chance? And this, herein lies the problem with Social Security. Social security, as we take this little exit ramp, was not built for longevity.

In 1881, Otto von Bismarck of Prussia. Prussia, Prussia. Is it Russia? Russia? Prussia? Prussia? Prussia? I don’t feel uncomfortable not knowing how to phrase that right now, because I feel like I have a good handle on global history, but I just don’t know if I’ve said that in a long time. He was the Prime Minister, and president of Prussia. Sorry, I keep wondering about that. And so, he came up with this idea, it was a radical idea, of retirement. And, of course, it was a socialist idea. And, you know, the idea of retirement was really like, if you were in, if you had a lot of money and you came from a rich family, it wasn’t really an issue.

But the problem is, is people who were poor, it was a really difficult dilemma. So, he created a retirement system for the people who are 70. And let me read a little bit about that system. Those who are disabled from work by age and invalidity, have a well-grounded claim to care from the state. It would take about eight years to work through their political system at the time, but by the end of the decade, the German government created a retirement system which provided for citizens over the age of 70. If they live that long.

The reality is they didn’t. So many people who were under this original system didn’t get much in benefits. Maybe a couple of years. The original system, by the way, Social Security was built on the backs of Otto von Bismarck. The system was designed for a few years. Now we’re talking 30 or 40 years. The system was not really designed for you to quit working and be retired, to be disposed of.

We are called to keep and cultivate the garden, and that has not changed. So when Gen X hits that magical age of 65, and it’s kind of an arbitrary age, I think we have to toss out those Morgan Stanley and Edward Jones commercials. We got to get those out of our heads. It’s kind of the modern-day salesman approach to this 1881 framework of Otto von Bismarck, and it really doesn’t work today.

But we do need to save. For Gen Xers, if we do think of it as a crisis, it’s very individualized, so we do need to save. We need to say for different reasons, just in case of dementia, stroke, we fall off a ladder, whatever our occupation is, we do need to save for that reason. And for that reason, saving for retirement has never been important. It’s just slightly a different reason for the MTV generation than it is for the baby boomers.

So, is it a retirement crisis? I don’t think so. I think it’s just going to be different than what we expected and what we’ve been sold. But I do believe that work is inherently good. And I do believe, and I have conviction that many of us in the Gen-X generation will need to pivot. And if we think about doing that well, I believe that not only will we be happier, but we’ll leave the world better than we found it. Thanks for listening today. And as always, you think different when you think long term. Have a great day.

Resources:

As Generation X Approaches Retirement, Reality Still Bites – WSJ

Does Work Make You Happy? Evidence from the World Happiness Report (hbr.org)

FastStats – Life Expectancy (cdc.gov)

Life-Planning in the Age of Longevity: Insights for Gen-Xers – Stanford Center on Longevity

How Retirement Was Invented – The Atlantic

Disclaimer: Clicking the Like button does not constitute a testimonial for, recommendation or endorsement of our advisory firm, any associated person, or our services. Clicking the Like button is merely a mechanism to circulate our social media page. “Like” is not meant in the traditional sense. In addition, postings must refrain from recommending us or providing testimonials for our firm.